The Strategic Deadlock: Why Victoria’s Tax Settings Are Exposing a Missing Layer of Property Strategy

In 2026, the economics of holding property in Victoria have fundamentally changed.

For decades, holding real estate was a forgiving strategy. Capital growth often masked inefficiencies, allowing underutilised assets to remain in portfolios without immediate consequence.

That is no longer the case.

Why This Is Intensifying Now

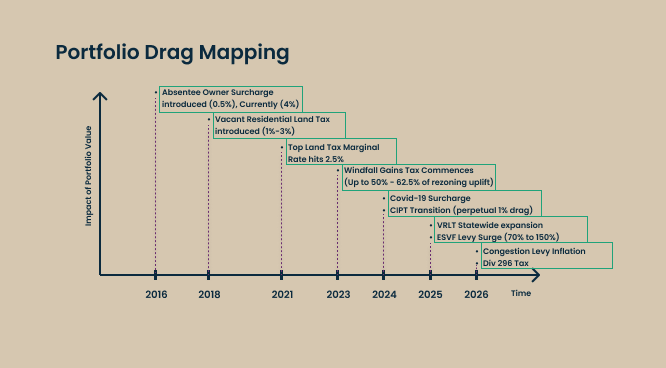

Today, Victorian private investors are facing a materially higher cost of holding property. The transition to Commercial and Industrial Property Tax (CIPT), Vacant Residential Land Tax, Absentee Owner Surcharges, the impending Division 296, and Windfall Gains Tax are increasing the carrying costs of underperforming assets. What was once neutral is now, in many cases, a drag on capital.

The current environment is not defined by a single change, but by the cumulative effect of several.

The Obsolescence Trap

The current cycle is driven as much by asset obsolescence as by tax pressures. Creeping obsolescence manifests in the divergence between prime and secondary assets. This gap is reflected in widening yield spreads and starkly different leasing outcomes.

Regulatory obsolescence continues to be a risk factor following the previous expansion of the Commercial Building Disclosure (CBD) Program, and potential future expansions of mandatory disclosure cannot be discounted. The threshold for mandatory NABERS (National Australian Built Environment Rating System) disclosure reduced from 2,000 square metres to 1,000 square metres several years ago.

Applicable buildings with poor energy efficiency (sub-4 stars) are increasingly treated as stranded assets, and this has become more relevant as existing tenant leases come up for expiry. Such buildings are becoming effectively barred from a tenant pool that includes government bodies, ASX-listed entities, and any corporation with a net-zero policy, as these occupiers cannot, by policy, lease non-compliant space.

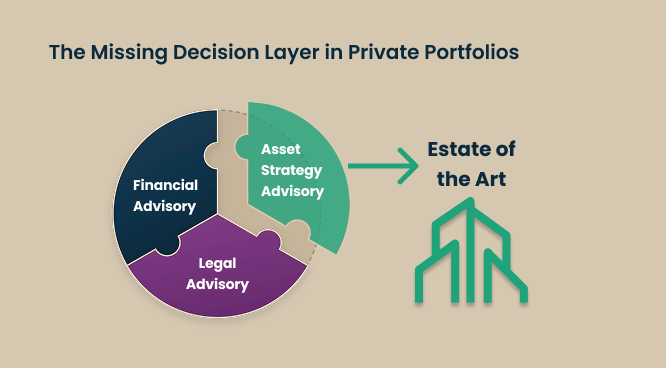

The Advisory Gap in the Private Portfolio

In many private portfolios, the gap is not capability, but responsibility.

Accountants manage the tax position. Lawyers manage structure and risk but responsibility for deciding what an asset should become is often unclear.

Property managers and leasing agents operate within the current state of the asset. They are not tasked with questioning whether that state should change.

As the private investor market increases in sophistication, institutional type frameworks are being adopted to manage their real estate exposure.

This evolution of capability does not replace existing operational specialists but provides the overarching strategic guide they need to be effective.

Whether sourced internally or through independent external advisors, establishing this dedicated layer of strategy ensures the operational engine is actively driven towards a specific destination rather than defaulting to a passive holding pattern.

What This Looks Like in Practice

In practice, a gap shows up in consistent ways. Three scenarios which we have come across are outlined below:

Scenario 1: The Industrial Property

A private family owns a 5,000 square metre industrial lot in the inner north, improved by an older 1,000 square metre warehouse leased to a long-term tenant. The rent is stable, and the property has been in the family for decades.

The Problem: The asset has a low site coverage (20%). The land value is high, but the building is functionally obsolete; it lacks the height, site configuration, and power capacity for modern logistics.

The Operational Reality: The incumbent property management framework is oriented towards immediate cash-flow preservation and tenant retention. Consequently, the default recommendation is to negotiate a standard lease renewal to secure the passing income.

The Strategic Reality: The issue is not leasing performance. It is that the asset’s low site coverage and rising land-based costs are not being tested against alternative uses or capital reallocation.

An Asset Stewardship Audit would model the "Highest and Best Use" (HBU) and show that a divestment now could potentially fund two modern, pre-leased industrial units in a growth corridor with a 200-basis point higher net yield.

Scenario 2: The Suburban Office

An investor owns a 2,500 square metre office building in a middle-ring municipality like Whitehorse or Monash. The building is well-maintained but has an old HVAC system and a 3-star NABERS rating.

The Problem: The mandatory disclosure threshold dropped to 1,000 square metres some years ago. The building’s largest and longest standing tenant is an insurance firm that has recently implemented a global "net zero" policy

The Operational Reality: The standard operational response has been to use incentives and minor capex to retain tenants.

The Strategic Reality: Without holistic capital restructuring to elevate the asset’s base building NABERS rating, the property faces structural tenant exclusion. The asset risks becoming stranded as it is permanently removed from the procurement parameters of institutional government and the increasing number of ESG driven occupiers irrespective of the magnitude of commercial incentives offered.

A Strategic Review would identify this risk early, informing either a divestment or a clear repositioning pathway.

Scenario 3: The Retail Strip

An investor owns a secondary retail strip in a high-amenity Municipality like Yarra, Boroondara, or Stonnington. Several shops are under-leased or on month-to-month tenancies, with management focused on incremental leasing to fill the gaps, which has been successful.

The Problem: While the property still generates passing rent at market rates, the owner absorbs rising land tax and, where applicable, the newly expanded Category 2 Congestion Levy.

The Operational Reality: The management approach is focused on maintaining income within the existing configuration of the asset. This sustains cash flow but does not address the underlying land value or planning uplift.

The Strategic Reality: With the gazettal of Amendment GC270 in March 2026, the property has moved into a "Core Activity Centre" or a "Housing Choice and Transport Zone." The true value no longer lies in the passing rent of secondary retail, but in the now permitted planning uplift.

In each case, the core vulnerability is not poor operational management. It is the absence of a clear, overarching strategic decision regarding the asset’s future role and highest and best use within the portfolio.

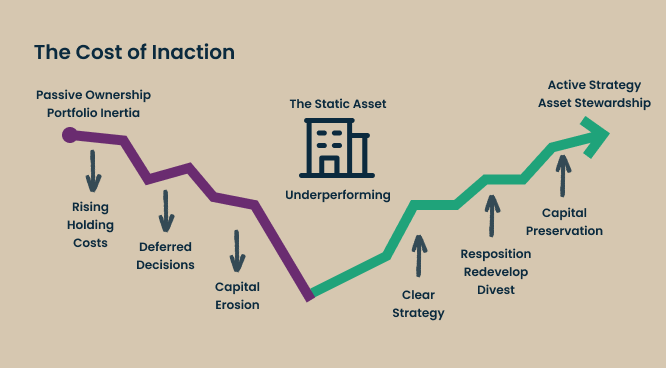

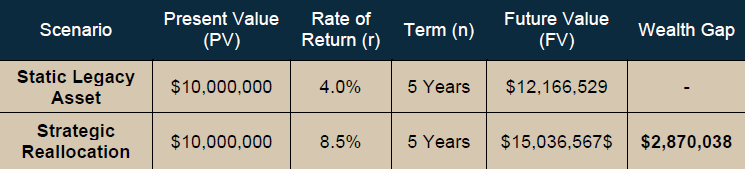

The Opportunity Cost of Static Capital

One of the more persistent assumptions in property investment is that long-term holding is inherently low risk. In practice, that assumption breaks down when capital is misallocated.

The cost of static capital is not just the return an asset generates, but the return it prevents elsewhere. Where capital is tied up in underperforming assets, investors forgo the ability to redeploy into higher-performing or more strategically aligned opportunities.

In previous cycles, this trade-off could be deferred. In the current environment, it is harder to justify. Rising holding costs and asset obsolescence mean that inaction is no longer neutral.

This becomes clearer over time.

The Missing Decision Layer

These are not purely tax or legal questions. They are decisions about the future role of an asset within a portfolio. Making them requires a level of objectivity that is often difficult when assets have been held for a long time, or when advice is fragmented across multiple disciplines.

In many private portfolios, this decision layer is informal or absent.

As a result, assets are often held by default rather than through deliberate strategy.

But in current market conditions, that avoidance is actively destroying yield. Breaking this holding pattern requires objectivity.

The Solution: Independent Strategy and the Asset Stewardship Audit

At Estate of the Art, we provide independent property expertise for private investors, facilitating a dedicated layer of portfolio and asset-level strategy.

We deliver this through the Asset Stewardship Audit, a structured assessment designed to determine the role a property should play within a portfolio.

The diagnostic provides clarity across four key areas:

Statutory and Holding Cost Exposure

A clear view of current and future holding costs and implications.Strategic Asset Potential

An assessment of whether the assets highest and best use differs from its current state.Capital and Compliance Requirements

An outline of capital required to maintain competitiveness and steps required to reposition the asset.Commercial Pathway Options

A comparison of viable options including hold, reposition, joint venture or divestment.

Once a direction is established, we act as the informed client on your behalf, translating strategy into clear mandates for agents, planners and advisers.

The question is no longer simply whether an asset is performing, but whether it remains fit for purpose within the portfolio.

If you are reviewing a legacy asset or portfolio position, we would welcome a confidential discussion on whether an Asset Stewardship Audit would be useful.